$75K when you look at the funds (30+ in years past) the majority of it from the normal rates of interest—personal bank loan maybe not given fund, we buckled down, existed using one income and put the second money on student education loans. dos.five years later it actually was repaid. Following i proceeded to live frugally (consider a bit a lot better than given that graduate pupils yet not far) and you may saved having a deposit. I failed to raise our very own way of living top much off scholar college for more 4 ages if we finished—all of the so we could pay-off the individuals annoying loans and also have to the a monetary stronghold.

The problem is it is impossible within $200K+ HHI your OP owes absolutely nothing plus in 13 years they commonly magically score forgiveness. During the their earnings there has to be a good payment. Including, such plans change-over big date, thus much can take place inside the thirteen ages, meanwhile the interest is growing very fast as the OP will pay absolutely nothing (otherwise practically nothing). It is therefore really not extremely wise to never be focused on investing them off. To allow them to “have fun with the system” however, any absolutely nothing hiccup as well as might end up buying $400K+ and certainly will never be capable of one. Whereas from the their income, they’re able to belt off and you can pay-off the fresh new financing they really got.

It may sound as you would prefer to live in a world in which every one of what you determine is the case, however, luckily your requirements are not form fact. Thought reading in the income-driven installment agreements before speculating then.

As well as, at least one out of the four IDR agreements was legal, so good luck with some thing altering quick thereon one.

Better it’s absurd! What happened so you’re able to personal responsibility? Try not to need college loans you cannot afford to pay right back, it’s really quite easy

As of numerous disciplines Wanted certain level. Heck, is a good PT you now you would like an effective doctorate. As to why should not people remove them for a life of works it like and are usually effective in? Or must do?

Universities and you may Unis could down university fees. There may be lowest if any focus money. A lot of things you to don’t wanted men and women to give up on its community of preference.

Also, I’d choose see the bundle in which it pay actually $500/month therefore only disappears into the thirteen ages for the much for the financing

In my opinion there was a pleasurable typical here, as well as in the greatest world yeah men and women could sit in their school of choice free of charge and rehearse one to education to complete its industry of choice. But it is perhaps not the greatest business.

You will find perhaps not problem with it and do not comprehend the you prefer so you’re able to work away at life to repay particular lender that’s gouging customers, and you can settee it as “personal obligations

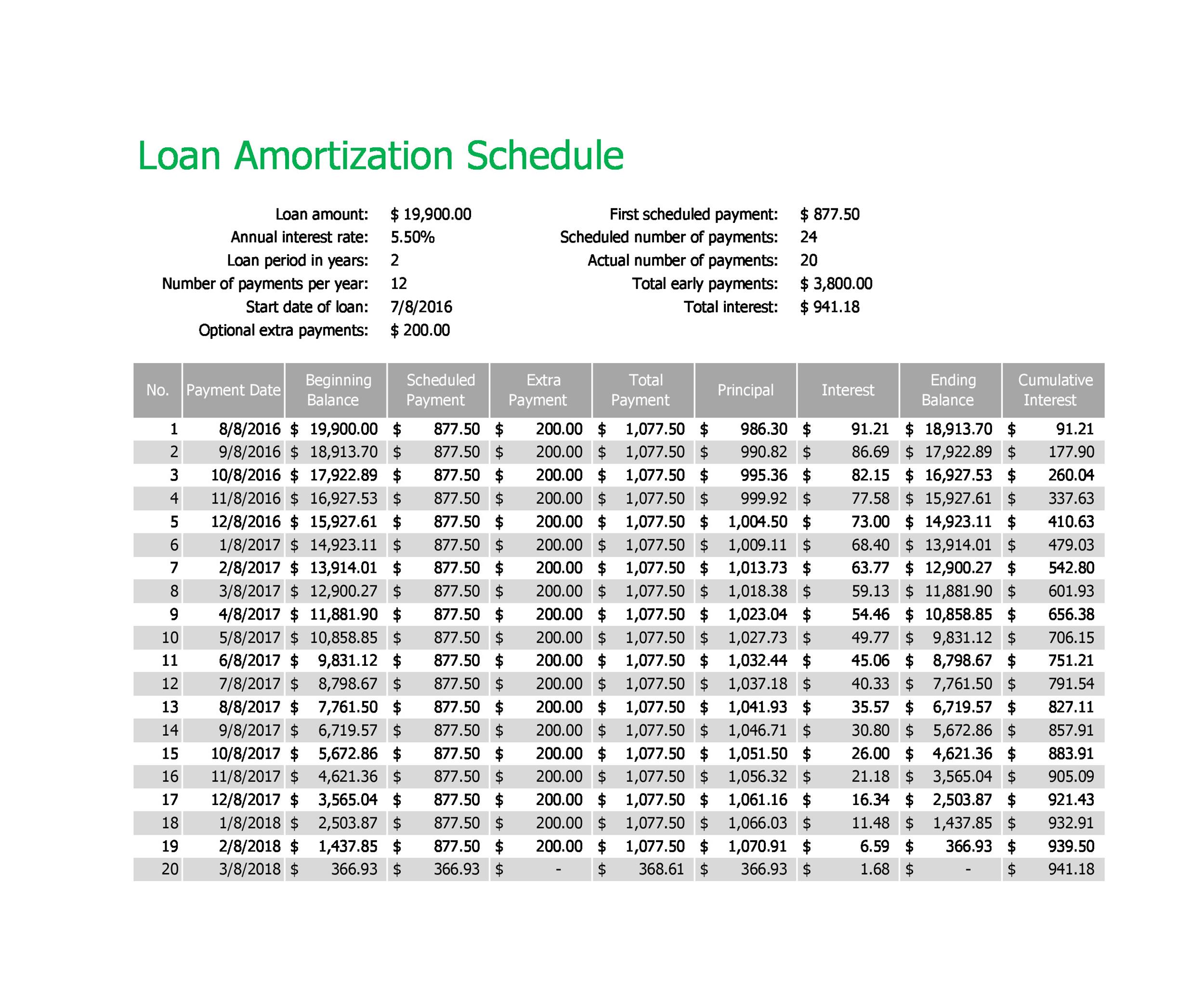

People including OP who has $220,000 indebted possesses a great HHI regarding $220,000 are using something towards the the individuals fund. And when $220,000 is the AGI the brand new calculator claims they should be expenses $1155-$1271 thirty day period.

Bookkeeping to have upcoming inflation, new expose well worth of the overall amount of cash might pay if financing was forgiven (thus and taxes to your forgiven equilibrium) would be on the $237,799. Which appears entirely reasonable to me.

Having them provides money within the-name-merely essentially which have $0 monthly obligations due to a world loophole how they are doing their fees (as this is the only way they’d end up with an effective $0 payment with the income and a good 4 people family with one to level of financial obligation) rubs me the wrong way. Specially when you may have anyone for https://speedycashloan.net/installment-loans-fl/ instance the PP that step one/next the amount of money and is using more than OP monthly. That’s the version of matter that really pisses individuals out of while the it’s not proper.